Sign up to receive daily news updates from CleanTechnica via email. Or follow us on Google News!

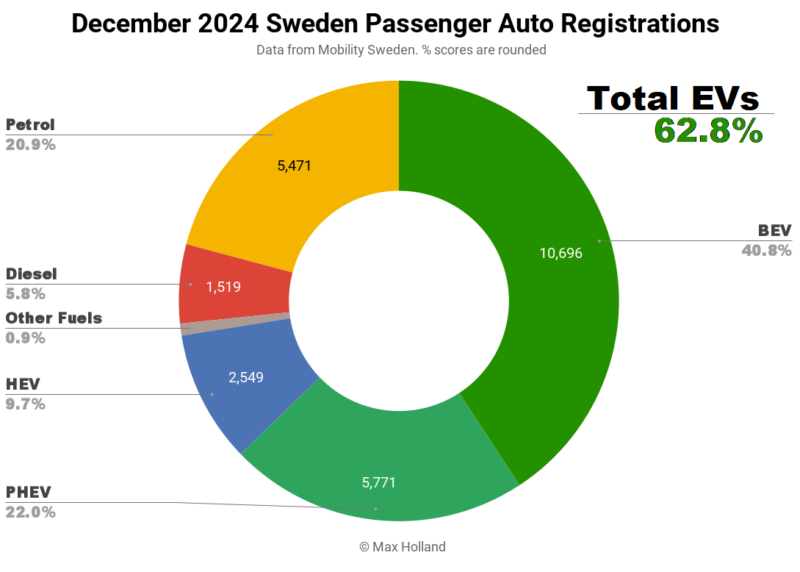

December saw plug-in EVs account for 62.8% of Sweden’s share, down slightly from 63.1% in December 2023. The EV share rose year-on-year (YoY), but was outweighed by a lower share of plug-in hybrid electric vehicles (PHEV). Total vehicle volume reached 26,237 units, down 10% year-on-year. The Tesla Model Y remained the best-selling electric vehicle for the eighth month in a row.

December car sales saw plug-in electric vehicles take a 62.8% share in Sweden, with full battery electric vehicles (BEVs) at 40.8% and plug-in hybrids (PHEVs) at 22.0%. These stocks compare year-over-year versus a combined 63.1%, with 38.9% BEV and 24.2% PHEV.

Full results for the year 2024

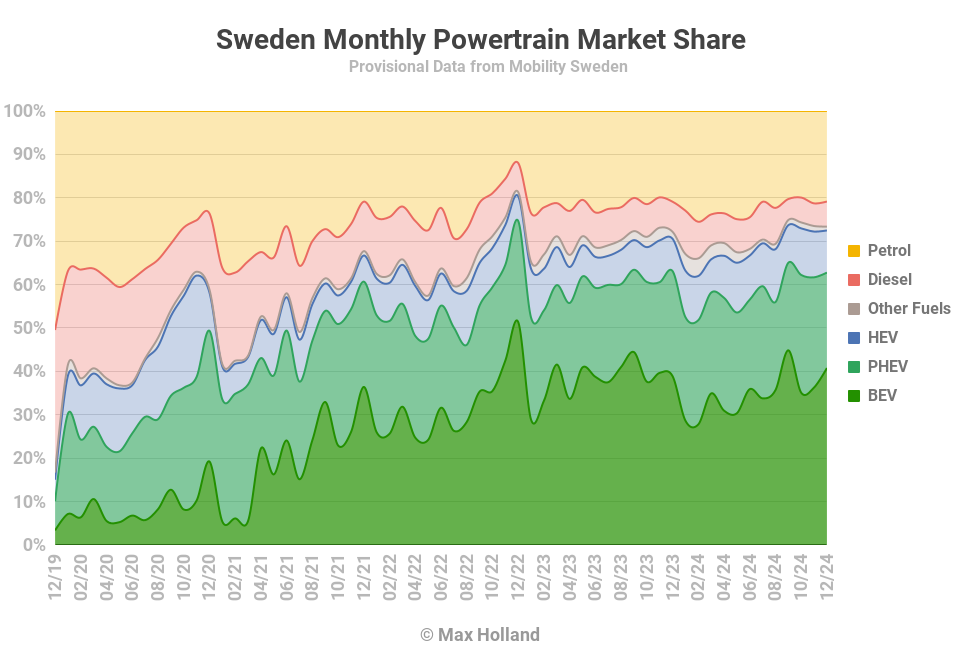

Sweden’s total vehicle market saw 269,500 sales in 2024, down 7% from 289,610 sales in 2023. Full-year powertrain shares for 2024 were 35.0% BEV, 23.4% PHEV, 10.1% HEV, 22 .5% gasoline, 7.0% diesel. This is comparable to the equivalent 2023 shares of 38.7% of EVs, 21.1% of PHEVs, 8.1% of PHEVs, 21.6% of gasoline, and 8.2% of diesel.

The trend was notably negative for battery electric vehicles – losing a significant 3.7% slice of the market pie – and slightly positive for plug-in hybrid electric vehicles. Combined, plugins actually lost 1.4% of their market share (from 59.8% to 58.4%). Meanwhile, hybrid electric vehicles gained an additional 2% share, gasoline rose only 1%, and diesel lost more than 1%.

The best we can say is that ICE-only vehicles have remained roughly constant, but battery electric vehicles have lost significantly to both hybrid and plug-in hybrid electric vehicles (almost equally). This is clearly a poor performance from an electric vehicle transition perspective.

One could point the finger at the removal of the incentive to buy EVs (for future orders) towards the end of 2022. This means that the first half of 2023 will still see reasonable volumes of EVs (deliveries that fulfilled orders placed before the November 2022 cut). However, nearly all BEV pre-orders were delivered by Q4 2023, however, BEV volume in Q4 2024 was 8% lower than this baseline.

This therefore suggests that incentive cuts were likely not the primary reason for EV weakness in 2024, and instead the main factors were likely continued consumer fatigue from a prolonged period of economic belt-tightening over the past couple of years, coupled with EV increases in The last two years. The price during the same period is still much more expensive than other engines.

December until 2025

The monthly result for December saw a roughly 6% decline in EV volume year-on-year, a slightly better performance than the overall decline in the auto market (10%), although PHEVs performed worse than the broader market, Down 19% year-on-year.

The only thing we have to look forward to from now on is a tightening of vehicle emissions regulations in the EU region in 2025. These regulations should see average fleet CO2 emissions fall by 15% compared to 2021 levels. The main goal was For this year it is 95 grams per kilometer of carbon dioxide, but it has allowed significant fraud. The period 2022-2024 stuck to the target of 95 g/km, but tightened the manipulation. 2024 was the final year of this relatively lax regime. There will likely be some progress in ICE-only sales (“clearing shelves”) through Q4 2024, and some EV deliveries delayed until 2025, to help get a head start on meeting 2025’s 15% tighter fleet-requirements level.

The main target for 2025 is (on average) “81 g/km CO2”. Although again some manipulation is allowed to sweeten the pill. This equivocation will intensify again as we head towards the next major target set for 2030. The 2030 target is a 55% reduction compared to 2021, with a headline of CO2 emissions of “43g/km”. Again, there will likely be some manipulation in the initial phase to help the medication go down.

During the recent period 2021-2024, legacy automakers kept the prices of battery electric cars high and deliberately slowed the transition process. They were also deceptively using the results of their slow strategies to claim that “the market” was not ready. They then in turn take the “market not ready” claim and put pressure on European policymakers to relax the requirements in the future!

This is all a somewhat predictable, cynical trick by Legacy Auto. We know that they have deliberately kept the prices of BEVs high and out of reach of many consumers (who have been clamoring for years for affordable BEVs).

Legacy auto battery electric cars should be much lower in price now. BEVs are already driving down the prices of ICE vehicles in almost all segments in China. In Europe, legacy cars have kept their EV prices high in order to extract more economic rents from their previous investments in ICE (and pay record dividends for themselves) while they still can, to the detriment of European consumers switching to electric cars. Their fossil fuel train is coming to an end, but we should expect their shenanigans to continue all the way into 2030 (and beyond).

Best selling electric cars

The Tesla Model Y was – as expected – the best-selling electric car in December once again, its eighth straight month in the top spot. Its volume, at 2,123 units, is almost identical to the next four models combined.

The Volvo EX30 ranked second with 753 units. Third place went to Volkswagen ID.7.

Just outside the top three, the Polestar 2 beat its recent averages and took fourth place, one unit ahead of the Volvo EC40.

Looking back, the new Kia EV3 saw a strong performance in just its third month on sale, finishing in 11th place (with 199 units), compared to 18th place in November. The new Cupra Tavascan also performed well, climbing to 15th place in its fifth month on sale, with 180 units in December. Finally, Zeekr

There was just one appearance in December, of the new Ford Capri, with an initial 38 units. The Capri saw its debut in neighboring Norway in October, so check out this report for a quick overview. Like its Ford Explorer sibling, the Capri is based on the Volkswagen Group’s MEB platform. It has not yet seen strong volumes in Norway, so don’t expect it to suddenly become a new favorite in Sweden either.

Like all manufacturers, Ford needs to meet stricter EU emissions regulations in 2025, as discussed above, and the Capri is a necessary step for them – we can expect its volumes to rise steadily from here.

Let’s check out the three-month rankings:

Here the top three are the same as in December’s rankings, although the Tesla Model Y isn’t quite as smug. The Volkswagen ID.7 rose 4 places from the previous period (Q3).

Most poses are mash-ups of regular faces, with a few exceptions. The Polestar 4 has performed well since its debut in July, now sitting in 10th place. It’s a similar story for the Audi Q6 (debut in June), which is now 14th, and the Porsche Macan (debut in September), which is now 17th. Finally, the Zeekr

There’s a good chance the Cupra Tavascan (debuting in August) will make it into the top 20 in the next month or two, starting from its current 26th position.

Here’s a quick look at the full-year 2024 results:

The Tesla Model Y clearly maintains the lead, but its weight has actually increased compared to 2023. The Volvo EX30 has been a huge success, taking second place in its first full year on sale.

Volkswagen’s ID.7 also had strong success, climbing to eighth place in its first full year. The Cupra Born performed relatively well (11th), and has now overtaken its cousin the Volkswagen ID.3 (13th).

A decline was seen in the BMW i4 (from 7th in 2023 to 17th in 2024), the Kia Niro (from 8th to 18th) and the Audi Q8 e-tron (from 17th to 28th). A significant decline was seen for the BYD Atto 3, which was in 11th place at the end of 2023, but only 52nd at the end of 2024. This is due to BYD’s strategic caution, and not to any problem with the car (which sold hundreds of thousands of units worldwide in 2024). Sweden’s loss is the Global South’s gain.

As also noted in Norway’s latest report, the Nissan Leaf is getting older, and falling in Sweden as well, from 15th in 2023 to 39th in 2024.

Which models do you expect to make a big splash in 2025? Let us know in the comments.

Expectations

As mentioned earlier, the Swedish economy has been rather weak over the past couple of years, which is certainly sapping consumers’ stamina and willingness to spend on big-ticket items like (deliberately overpriced) battery electric cars. The latest GDP data is still from the third quarter, and was 0.7% year over year. Interest rates fell to 2.5% in December, and inflation remained low at 1.6%. Consumer confidence was negative at 96.7 points. The manufacturing PMI fell to 52.4 points in December, from 53.8 points in November.

Overall, 2024 was certainly a year to forget for Sweden’s electric vehicle transition, and we have to look forward to tightening emissions regulations in 2025 to get it back on an upward trajectory.

What are your thoughts on what we might see in 2025? Please join the conversation in the discussion section below.

Get a few dollars a month to help support independent cleantech coverage that helps accelerate the cleantech revolution! Do you have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here. Subscribe to our daily newsletter to get 15 new clean tech stories every day. Or sign up for our weekly program if daily is too frequent. advertisement

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica comment policy